2025 Global Mining Project Spending Outlook

Xuan-Ce Wang

1/30/20254 min read

As we enter 2025, the global mining industry continues to experience robust project spending. Equipment and service providers have benefited from a seven-year growth period, during which project spending has more than doubled since the market bottomed out in 2017. Between 2017 and 2024, capital expenditures among eight major mining companies (Anglo American, Barrick, BHP Group, Freeport-McMoRan, Glencore, Newmont, Rio Tinto, and Vale) increased from $23.9 billion to $48.4 billion. This expansion has been driven by key trends such as the energy transition, resource security, decarbonization, and productivity optimization, all of which will continue to influence investment decisions in 2025.

However, project spending may peak and moderate this year due to factors such as fluctuating base metal prices and a slowing energy transition. Global GDP growth in 2025 is projected to be moderate, with economic indicators suggesting stable but restrained project momentum compared to previous years. China, which consumes half of the world’s commodities, remains a significant factor, as its economic slowdown affects metal and mineral demand. Additionally, increased supply from new mines—especially for battery metals such as lithium, nickel, and cobalt—combined with lower-than-expected electric vehicle adoption in the West, is impacting short-term market dynamics. Many of these new mines, primarily in China or controlled by Chinese corporations, have led to project delays or cancellations. Nevertheless, strategic investments in the U.S. and EU, supported by government incentives and trade policies, will drive continued activity in critical minerals.

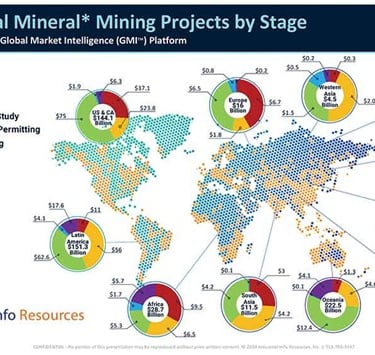

1. Global Critical Mineral Mining Landscape

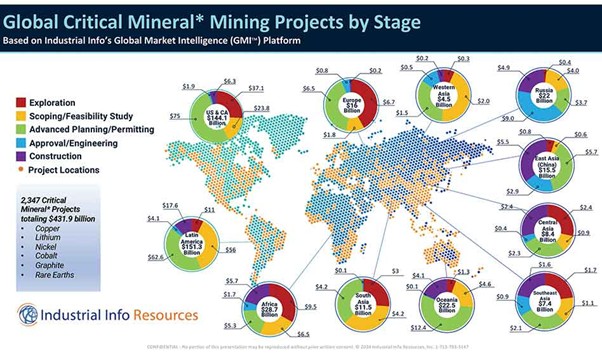

There are over 2,300 active critical mineral projects worldwide, totaling $431.9 billion. The Americas hold a dominant position, accounting for 68% of project value, with Latin America and North America leading in investment. Africa and Oceania also hold significant shares of project spending. The energy transition and decarbonization efforts are key drivers of demand, leading to continued mining expansions and new project commitments despite near-term market fluctuations. However, long permitting processes and stringent ESG requirements push companies to prioritize optimizing and expanding existing operations. AI and automation are playing an increasing role in improving operational efficiency, reducing costs, and enhancing safety and exploration efforts.

2. Energy Transition and Its Impact on Mining

The demand for electrification metals is expected to surge due to power infrastructure expansion and data center growth. Industrial Info’s Global Market Intelligence (GMI) reports over 3,700 active data center projects, representing approximately $890 billion in investment and requiring 112 gigawatts of electricity. This trend will drive demand for steel, copper, aluminum, and other metals essential for electrification. While renewable energy sources like wind and solar will continue to expand, natural gas and nuclear power are gaining traction as stable baseload solutions. The growing interest in small modular reactors (SMRs) is boosting uranium demand, leading to a resurgence in dormant mining projects.

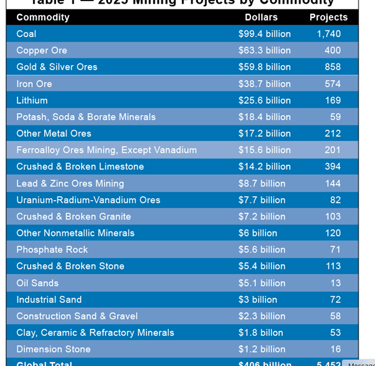

3. 2025 Mining Project Pipeline

According to GMI, over 5,400 mining projects worth $406 billion are set to begin construction in 2025. However, many of these projects may face delays or cancellations due to regulatory, financial, and market-related challenges. Despite this, coal remains the leading commodity in terms of project activity, accounting for nearly 25% of total investment. China dominates the coal sector, followed by India, Indonesia, and Australia. Meanwhile, copper projects are poised for substantial growth, driven by increasing demand from electrification trends. Notable projects include Barrick’s $4 billion Reko Diq copper-gold project in Pakistan and a surge of new copper developments in Argentina, spurred by favorable investment policies.

4. Key Commodity Trends

Gold: With prices surpassing $2,700/ounce in late 2024, gold remains a preferred investment in uncertain geopolitical times. Canada, the U.S., and Peru lead in gold mining project activity.

Iron Ore: After years of expansion, iron ore project activity has slowed, particularly in Australia and Brazil, due to declining demand in China.

Lithium: The market faces oversupply challenges, with lithium prices dropping significantly. High-cost producers, including some Australian spodumene miners, have scaled back operations, while government-supported projects in Finland and Nevada continue moving forward.

Nickel: Price volatility has led to project cancellations and delays, particularly in Indonesia, the world’s largest nickel producer.

5. Regional Outlook

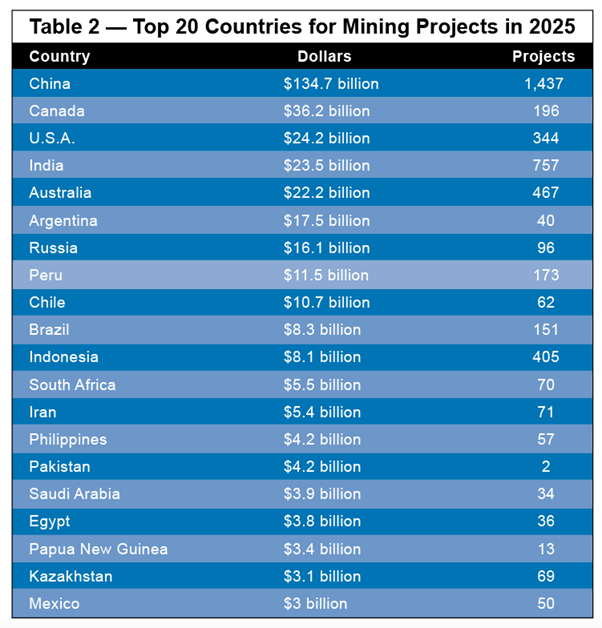

China leads global mining project activity, with over 1,400 projects worth $134.7 billion, primarily in coal and iron ore. Canada and the U.S. follow closely, with strong investments in critical minerals and gold. India is emerging as a major player, particularly in coal and copper. Australia, once a leader, has slowed due to reduced demand for its coal and iron ore exports. Indonesia remains active in coal and gold mining, while Middle Eastern nations such as Iran, Saudi Arabia, and Egypt are ramping up mining investments to diversify their economies.

6. Conclusion

While mining project activity in 2025 may stabilize, it remains nearly double the levels seen in 2017. The slowdown in the energy transition and increased supply competition may cause some delays, but the industry stands to benefit from rising demand linked to data center expansion, electrification, and decarbonization efforts. Trade uncertainties and geopolitical tensions will continue to drive investments in domestic supply chains for critical minerals. Additionally, AI and automation will play an increasingly significant role in enhancing efficiency, safety, and cost management in existing mines. The mining industry is poised for continued growth, albeit with a more strategic and selective approach to new project development.