Copper: The Next Oil? Analysis of Future Demand in the Energy Transition

Xuan-Ce Wang

4/28/20253 min read

Abstract

This paper examines the projected surge in copper demand through 2040, analyzing the parallel decline in oil consumption and the implications for global markets, energy transition policies, and resource security. As the world moves toward net-zero emissions goals, copper emerges as a critical resource whose supply-demand dynamics may mirror oil's historical economic significance.

Introduction

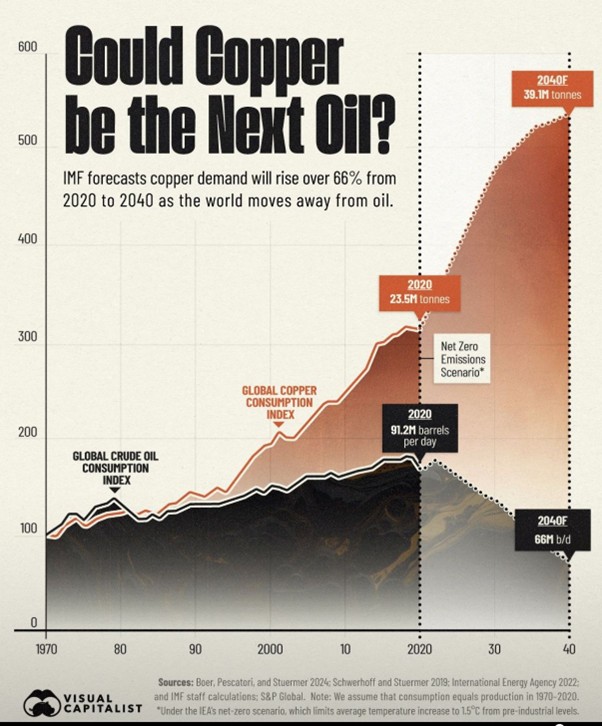

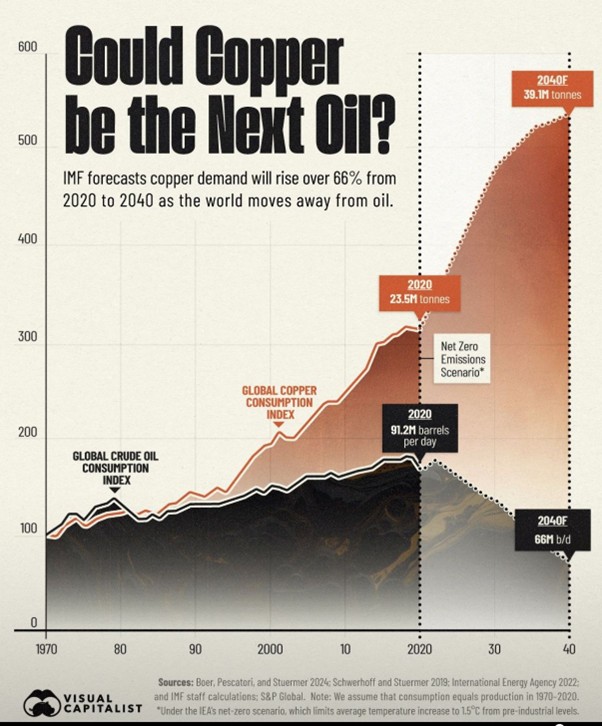

The global shift away from fossil fuels toward renewable energy technologies has created unprecedented demand for specific minerals and metals. Among these, copper stands out as particularly critical due to its extensive applications in electrical systems, renewable energy infrastructure, and emerging technologies. The International Monetary Fund forecasts that copper demand will rise over 66% from 2020 to 2040, raising questions about copper's potential to become as economically and geopolitically significant as oil has been for the past century.

Key Findings from Data Analysis

Diverging Consumption Patterns

As illustrated in the accompanying figure, copper and oil consumption trends show a striking divergence beginning around 2020, with copper demand projected to increase dramatically while oil consumption declines:

• Copper Consumption:

2020 baseline: 23.5M tonnes

2040 forecast: 39.1M tonnes (66% increase)

Shows consistent growth since 1970 with accelerated trajectory post-2020

• Oil Consumption:

2020 baseline: 91.2M barrels per day

2040 forecast: 66M barrels per day (28% decrease)

Growth peaked around 2020, with declining consumption under net-zero scenarios

Historical Context (1970-2020)

The figure demonstrates that both copper and oil consumption grew throughout the period from 1970 to 2020, with copper consumption showing a steeper growth trajectory, particularly after 2000. This correlation reflects global industrial development and economic growth patterns over this period.

The 2020 Inflection Point

The year 2020 marks a critical inflection point where:

1. The COVID-19 pandemic temporarily disrupted global supply chains

2. Climate policy commitments accelerated

3. Renewable energy costs reached parity with fossil fuels in many markets

Net-Zero Emissions Scenario

Under the International Energy Agency's net-zero scenario (limiting average temperature increase to 1.5°C from pre-industrial levels), the divergence between copper and oil becomes most pronounced:

Copper demand accelerates even more steeply

Oil demand decreases substantially from previous peaks

Driving Factors of Copper Demand Growth

Electrification of Transportation

The transition from internal combustion engines to electric vehicles represents a significant driver of copper demand:

• An average electric vehicle requires 2.5-3 times more copper than a conventional vehicle

• Charging infrastructure adds additional copper requirements

• Public transportation electrification (buses, trains) is copper-intensive

Renewable Energy Expansion

Renewable energy systems require substantially more copper than conventional power generation:

• Solar PV systems: 5-6 times more copper per megawatt than natural gas plants

• Wind power: 3-4 times more copper per megawatt than conventional generation

• Grid infrastructure reinforcement to accommodate distributed generation

Smart City Infrastructure

The development of smart and sustainable cities further drives copper demand:

• Smart grid technologies

• Energy-efficient buildings with advanced electrical systems

• Urban electrified transportation systems

Emerging Market Development

Continued industrialization and urbanization in emerging economies will maintain baseline demand for copper in traditional applications alongside green technology growth.

Supply-Side Challenges

Resource Constraints

Unlike oil, which faces demand challenges, copper faces supply constraints:

• Declining ore grades in existing mines

• Increasing depths and complexity of new mining projects

• Geographic concentration of reserves in politically sensitive regions

• 10-15 year average development timeline for new mines

Investment Gaps

Current investment in copper mining capacity appears insufficient to meet projected demand:

• Estimated $100-150 billion investment needed by 2030

• Project delays due to environmental and social permitting challenges

• Investor hesitancy due to historical commodity price volatility

Recycling Limitations

While copper is highly recyclable:

• Collection and processing infrastructure remains underdeveloped in many regions

• Growing demand outpaces recycling capacity

• Quality requirements for certain applications limit recycled content

Policy and Market Implications

Price Dynamics

The projected supply-demand imbalance suggests potential for:

• Sustained higher copper prices compared to historical averages

• Increased price volatility during transition periods

• Price signals driving investment in mining, recycling, and substitution

National Security Considerations

As with oil, copper resources may become a matter of national security:

• Resource nationalism in copper-rich nations

• Strategic reserves development in import-dependent countries

• Trade policies focusing on securing supply chains

Innovation Drivers

Price pressures may accelerate:

• Material substitution research for certain applications

• Mining technology innovation to access lower-grade resources

• Recycling technology and infrastructure development

Conclusion

The data presented in the figure and supporting research suggest that copper is indeed poised to become a resource of similar economic significance to oil, albeit for different reasons. While oil's importance stemmed from its irreplaceable role as an energy carrier, copper's criticality will derive from its essential function in enabling the very transition away from fossil fuels.

As the world progresses toward net-zero emissions goals, policymakers, investors, and industry stakeholders must recognize the strategic importance of copper supply chains. Unlike the oil era, which focused on securing access to energy resources, the coming decades will require a focus on securing the materials that enable clean energy production and electrification.

The projected 66% increase in copper demand by 2040 presents both challenges and opportunities. Addressing potential supply constraints through timely investment, technological innovation, and policy support will be essential to prevent copper availability from becoming a bottleneck in the global energy transition.

References

• Boer, Pescatori, and Stuermer 2024

• Schwerhoff and Stuermer 2019

• International Energy Agency 2022

• IMF staff calculations

• S&P Global