Global Lithium Supply Chain: From Extraction to Battery Manufacturing

Xuan-Ce Wang

8/11/20254 min read

Executive Summary

The global lithium industry represents a critical component of the modern energy transition, powering everything from electric vehicles to smartphones and grid-scale energy storage systems. However, the current supply chain structure reveals significant concentration risks and geopolitical vulnerabilities that threaten long-term supply security for Western economies.

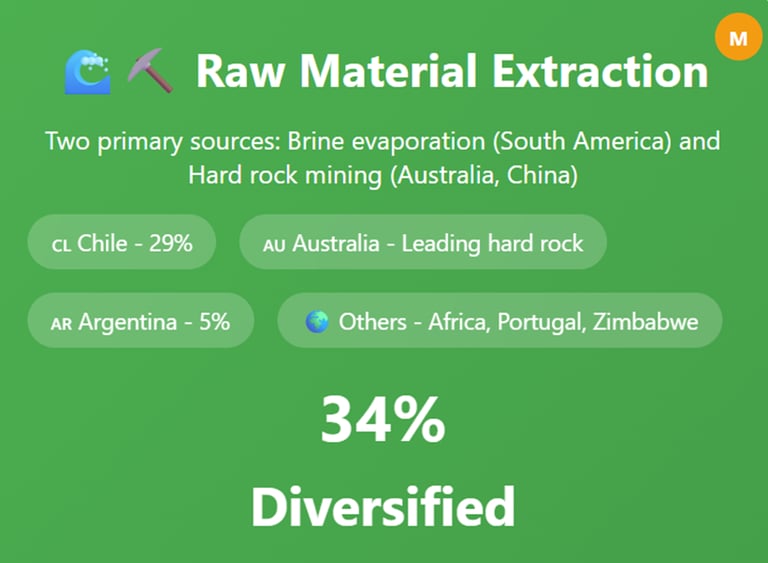

Lithium Extraction: Two Primary Pathways

Brine Evaporation

The traditional method involves extracting lithium from underground brine deposits, primarily concentrated in South America's "Lithium Triangle." This process requires large evaporation ponds where brine is pumped to the surface and allowed to evaporate over 12-18 months, concentrating the lithium content. While cost-effective, this method is water-intensive and weather-dependent.

Hard Rock Mining

The alternative approach involves extracting lithium from spodumene ore through conventional mining operations. Australia leads this sector, offering more predictable production timelines compared to brine operations, though typically at higher operational costs.

Global Mining Landscape

The current mining distribution reveals heavy concentration in a few key regions:

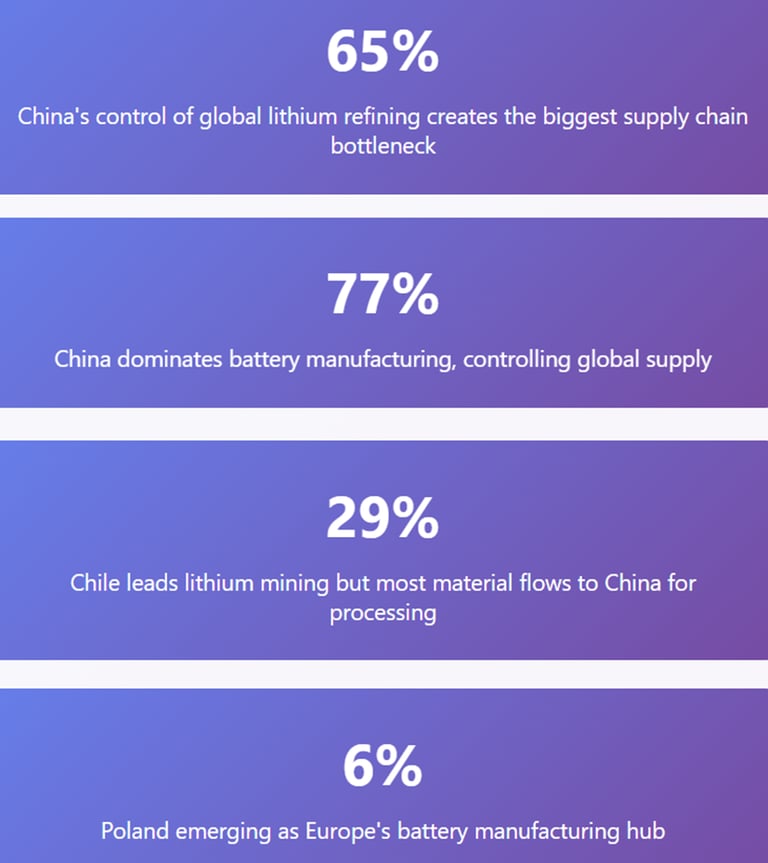

Chile dominates global production with 29% of worldwide lithium mining, leveraging its massive brine reserves in the Atacama Desert. The country's established infrastructure and favorable geology make it the current market leader.

Argentina contributes 5% of global production, with significant expansion potential as new projects come online in provinces like Catamarca and Jujuy.

Australia emerges as the hard rock leader, though often underrepresented in brine-focused statistics. The country's spodumene operations provide crucial supply diversification from South American brine sources.

Emerging players across Africa, China, and newer entrants like Portugal and Zimbabwe are developing projects that could reshape the supply landscape over the next decade.

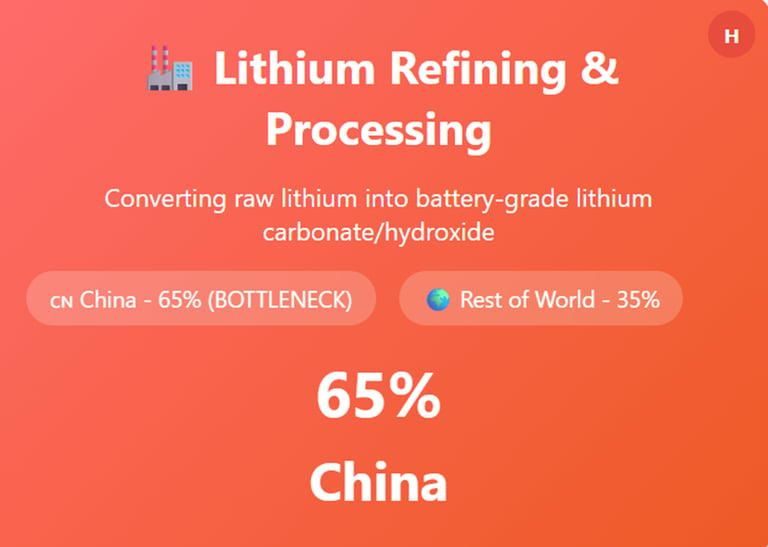

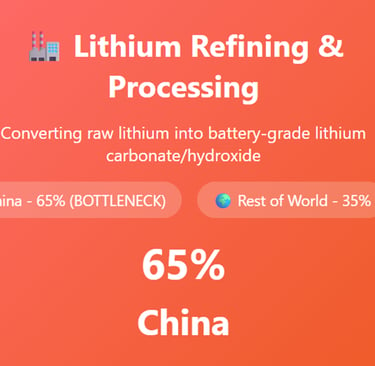

The Critical Refining Bottleneck

Perhaps the most significant vulnerability in the lithium supply chain lies in the refining stage. China controls an overwhelming 65% of global lithium refining capacity, creating a dangerous chokepoint between raw material extraction and battery-grade lithium production.

This concentration means that even lithium mined in Australia or South America often requires processing in Chinese facilities before becoming suitable for battery manufacturing. The refining process converts raw lithium into lithium hydroxide or lithium carbonate with the precise chemical specifications required for battery production.

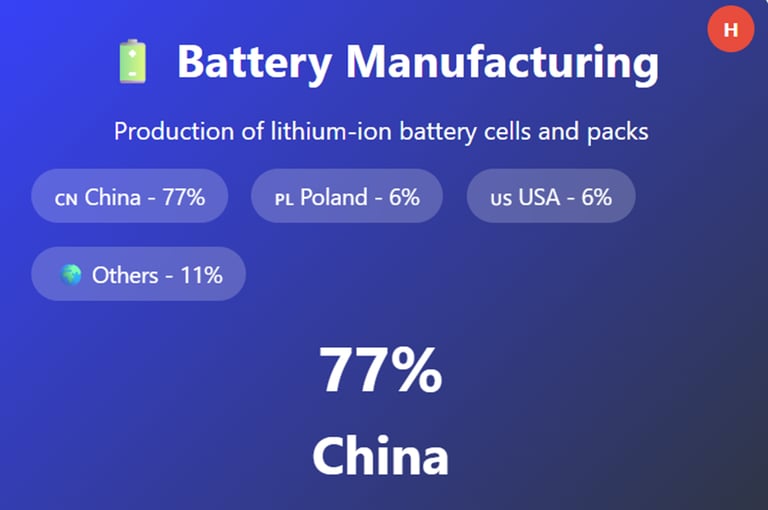

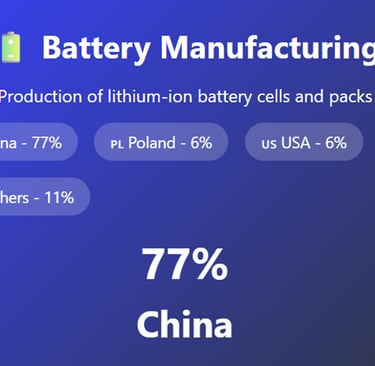

Battery Manufacturing Dominance

China's control extends beyond refining into battery manufacturing itself, where the country produces 77% of all lithium-ion batteries globally. This dominance spans the entire battery ecosystem, from cathode and anode materials to cell assembly and pack integration.

The remaining global production is distributed among:

Poland: 6% (emerging as Europe's battery hub)

United States: 6% (expanding through domestic initiatives)

Rest of world: 11% (scattered across various smaller producers)

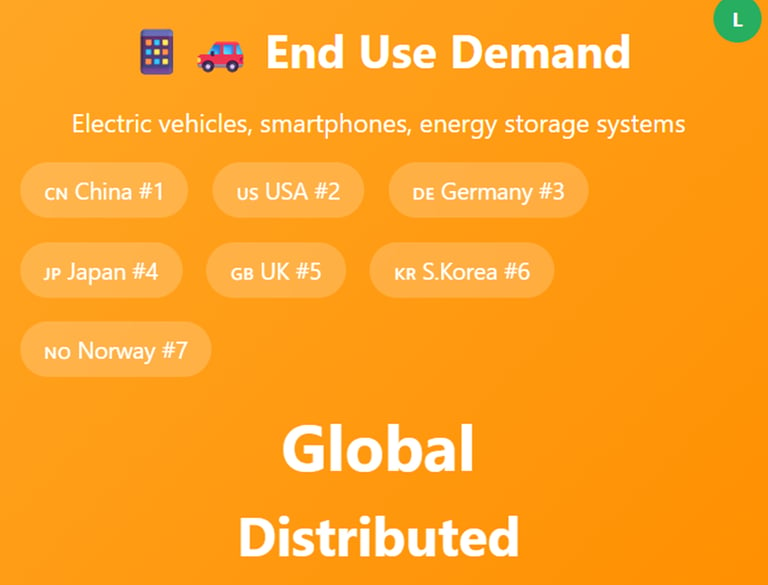

Global Battery Demand Centers

Battery demand concentration reflects the world's largest economies and their electrification ambitions:

China leads consumption, driven by massive domestic EV adoption and manufacturing export needs

United States represents the second-largest market, accelerated by federal EV incentives and infrastructure investment

Germany anchors European demand as the continent's automotive manufacturing center

Japan maintains significant demand through its advanced technology sector and hybrid vehicle production

United Kingdom shows growing demand driven by aggressive net-zero commitments

South Korea combines domestic consumption with significant battery export manufacturing

Norway demonstrates the highest per-capita EV adoption globally, creating outsized demand relative to population

Strategic Implications and Risks

Supply Chain Vulnerabilities

The current structure creates multiple points of failure. A disruption in Chinese refining capacity could paralyze global battery production regardless of upstream mining availability. Similarly, geopolitical tensions could weaponize these dependencies, as seen in other critical mineral supply chains.

Economic Security Concerns

Western economies face a strategic dilemma: their energy transition success depends on supply chains controlled by a potential economic rival. This creates both immediate supply risks and long-term economic dependency that could undermine energy security goals.

Environmental and Social Considerations

Lithium extraction, particularly brine operations, raises significant environmental concerns around water usage in already arid regions. Social impact on indigenous communities in South America adds another layer of complexity to supply chain ethics.

Strategic Questions for the Future

European Battery Independence

Europe faces a critical decision point regarding lithium refining capacity expansion. The continent currently imports most battery-grade lithium despite having domestic automotive manufacturers increasingly dependent on electric vehicle production. Building European refining capacity would reduce dependence on Chinese processing but requires significant capital investment and technical expertise development.

Poland's Battery Hub Ambitions

Poland's emergence as Europe's battery manufacturing center, capturing 6% of global production, positions the country as a potential regional leader. The question remains whether Poland can scale this position into broader supply chain integration, including upstream refining capabilities that would serve the broader European market.

Developing World Integration

Africa and Latin America possess substantial untapped lithium reserves but currently occupy primarily raw material export roles. Their potential evolution into value-added processing and manufacturing could reshape global supply dynamics while providing greater economic development opportunities for resource-rich nations.

Recommendations

Diversification Imperative: Western economies must prioritize supply chain diversification through strategic partnerships with non-Chinese producers and investment in domestic refining capacity.

Technology Investment: Advanced extraction and processing technologies could unlock new supply sources while reducing environmental impacts, particularly for brine operations.

Strategic Stockpiling: Given the concentration risks, strategic lithium reserves similar to petroleum stockpiles may become necessary for economic security.

Partnership Development: Deeper engagement with Latin American and African producers through technology transfer and infrastructure investment could create more balanced global supply chains.

Conclusion

The lithium battery supply chain represents both the foundation of the clean energy transition and a significant strategic vulnerability for Western economies. While current production meets global demand, the concentration of critical processing capabilities in China creates systemic risks that require coordinated policy responses. Success in managing these challenges will determine whether the energy transition enhances or undermines long-term economic and energy security.