The Great Copper Rush: How Tariff Fears Are Reshaping Global Metal Markets

Xuan-Ce Wang

6/16/20254 min read

The global copper market is experiencing an unprecedented disruption as traders and importers race against time to stockpile the industrial metal in the United States. This frenzied activity, driven by the looming threat of import tariffs under the Trump administration, is creating ripple effects across international markets and fundamentally altering global supply chains.

A Market in Upheaval

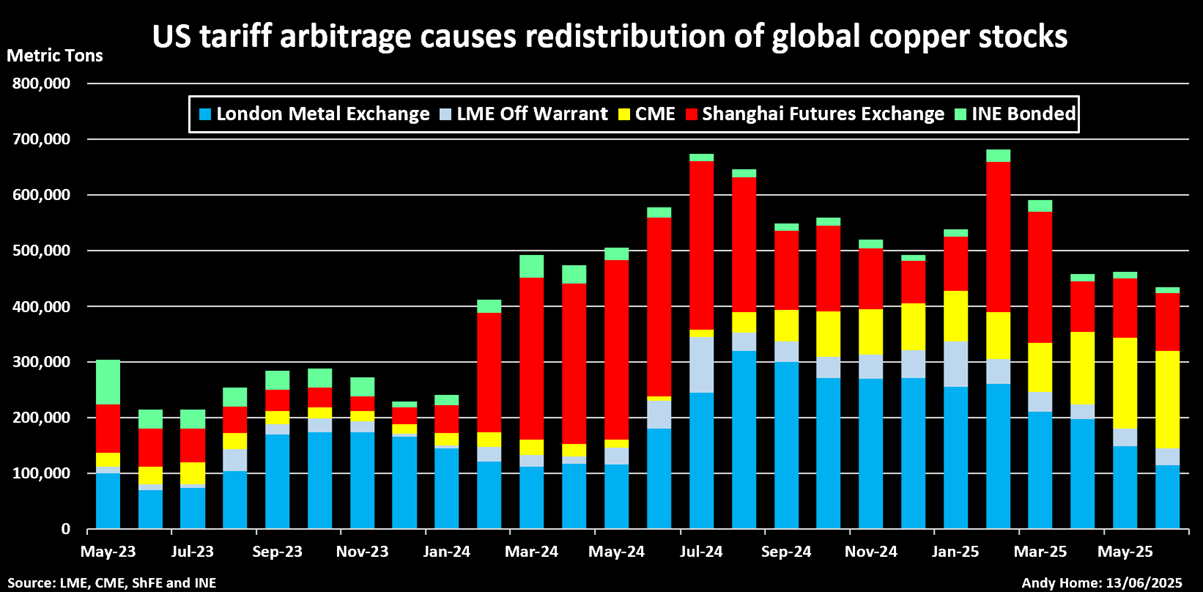

The collective scramble to move as much physical copper as possible to US shores before potential tariff implementation has created acute shortages elsewhere in the world. London Metal Exchange (LME) stocks have plummeted to nearly two-year lows, with time-spreads flaring into backwardation as inventory steadily drains away from traditional storage hubs.

This extraordinary redistribution of copper inventory will likely continue until President Trump's administration clarifies its position on whether copper will join the growing list of metals subject to punitive import duties. The uncertainty has created a market environment where traders are hedging their bets through physical positioning rather than waiting for policy clarity.

The Policy Backdrop

The Section 232 investigation launched by the administration in February operates under a 270-day deadline, creating a ticking clock that has intensified market activity. While administration officials have suggested the investigation would be completed in accelerated "Trump time," the market continues to operate in a state of suspended animation, pricing in potential scenarios while awaiting concrete policy decisions.

The CME customs-cleared US copper contract continues to command a substantial premium over the London market, with the arbitrage representing one of the most volatile yet profitable trades in the metals complex. At the current spread of approximately $1,000 per metric ton on a three-month delivery basis, traders appear to be pricing in a potential 10% tariff scenario.

Critically, this transatlantic price gap more than covers shipping and logistics costs, ensuring continued economic incentive for the physical copper trade from international markets to US storage facilities.

The Numbers Tell the Story

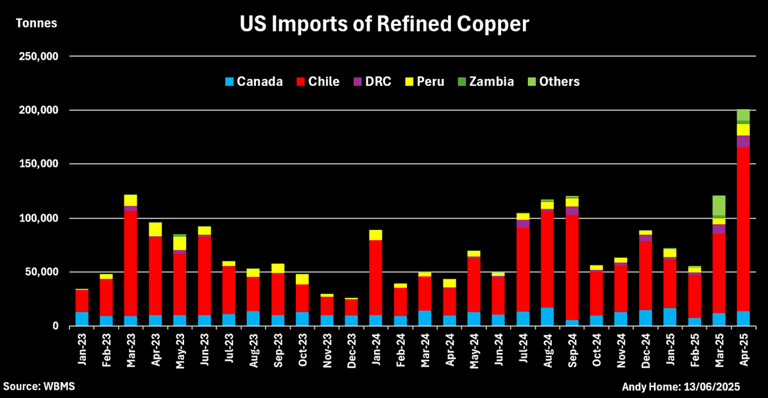

US refined copper imports have reached extraordinary levels, jumping to more than 200,000 tons in April alone—the highest monthly arrival rate recorded this decade. The cumulative impact is even more striking: imports totaled 455,000 tons in the first four months of 2025, representing more than double the tonnage imported during the same period in 2024.

This surge reflects not just increased demand but a fundamental shift in global copper flows, as market participants position themselves ahead of potential policy changes that could dramatically alter the economics of international copper trade.

Chile's Dominant Role

Chilean copper brands have emerged as the preferred choice for US importers, accounting for 61% of total inbound shipments in March and an overwhelming 75% in April. This preference is not coincidental—the CME's list of good-delivery brands includes 19 from Chilean producers, making Chilean copper the most readily acceptable for US exchange delivery.

The impact on LME inventories has been dramatic. LME warehouse stocks of Chilean-brand copper have been virtually eliminated, falling precipitously to just 75 tons at the end of May from 25,150 tons at the close of 2024. This represents a 99.7% decline in available Chilean copper within LME storage facilities.

The Chilean copper drain is also evident in Chinese import data, where imports of Chilean metal fell 44% year-over-year in the January-April period, even as total Chinese refined copper imports remained flat. This suggests that Chilean producers are actively redirecting their output toward the US market to capitalize on the premium pricing.

A Global Phenomenon

While Chile dominates the current import mix, the gravitational pull of the US tariff threat has attracted copper from an unprecedented range of countries. Nations that rarely ship to the US market—including Australia, Belgium, Germany, Spain, and South Korea—have all contributed to the import surge, highlighting the global nature of this supply chain reorganization.

Perhaps most surprisingly, Chinese trade figures suggest that even China has shipped close to 50,000 tons to the US market. However, this figure likely represents metal being stripped from bonded warehouses and re-exported rather than newly produced copper—a practice known as "turnaround" trading that China's customs department confusingly counts as an export.

Exchange Inventory Dynamics

The physical movement of copper is clearly visible in exchange warehouse data. CME inventory has been rising consistently, more than doubling this year to reach 175,954 tons as of the latest count. This represents a direct transfer of metal from international markets to US storage facilities.

Conversely, LME warehouses are experiencing steady depletion. More than half of the headline stocks of 114,475 tons have been cancelled in preparation for physical load-out, indicating that the outflow is likely to continue as long as the current economic incentives remain in place.

Market Implications

This copper redistribution represents more than a temporary trade opportunity—it signals a potential long-term shift in global commodity flows. The current situation demonstrates how policy uncertainty can create powerful economic incentives that reshape international supply chains, sometimes in ways that policymakers may not have initially anticipated.

For market participants, the lesson is clear: in an era of increasing trade protectionism, physical positioning ahead of policy implementation has become a crucial risk management strategy. The copper market's current dynamics may well serve as a template for how other commodity markets respond to similar policy uncertainties in the future.

As the Trump administration's 270-day deadline approaches, the copper market will continue to operate in this state of elevated activity. The ultimate resolution—whether copper faces tariffs or not—will determine whether this extraordinary redistribution of global copper inventory represents a temporary disruption or the beginning of a new era in international metals trading.